Pay in parts at Klarna

Shift from financing 1.0 and offer term loans (pay in parts) in Austria and Germany

Klarna’s old Financing account (revolving credit) let users bundle multiple debts and make minimum payments. It encouraged long-term debt and lacked transparency. With tighter regulations and a growing focus on financial responsibility, Klarna needed a clearer, more transparent alternative. The goal was to help users finance larger purchases responsibly while maintaining trust.

I led the design of Term Loans for Austria and Germany. I owned the purchase flow from research to launch, including flow mapping, high-fidelity designs, prototypes, user testings, and final implementation. I worked closely with engineering through weekly syncs, coordinated with legal, open banking, and underwriting teams, and partnered with a UX researcher from the localization team, on recruitment and testing. Along the way, I encountered different constraints like:

- Regulatory: strict transparency and credit standards

- Research access: no in-person testing; relied on remote studies and localization partners

- Cross-team dependencies: multiple teams needed alignment for one seamless experience

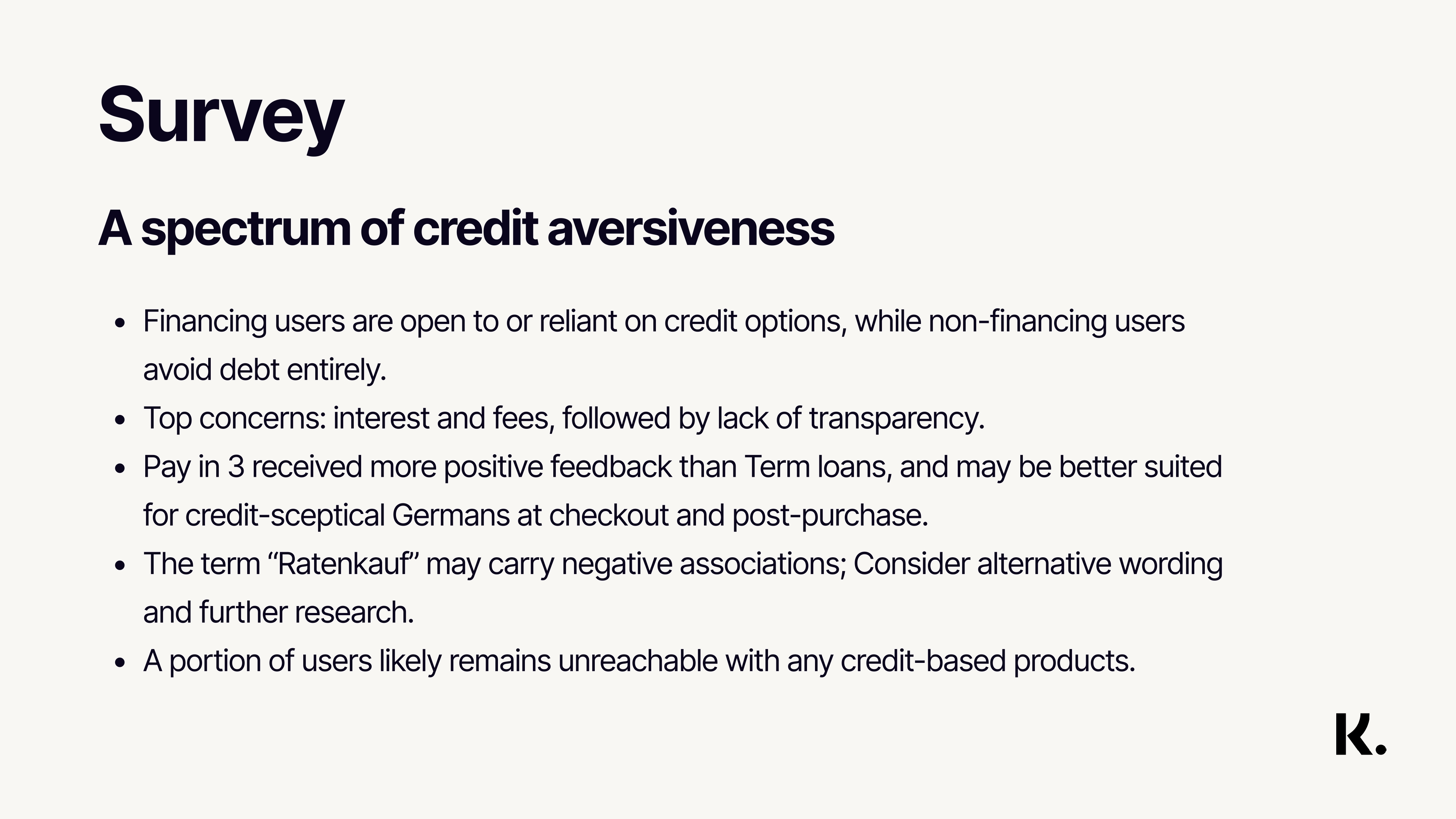

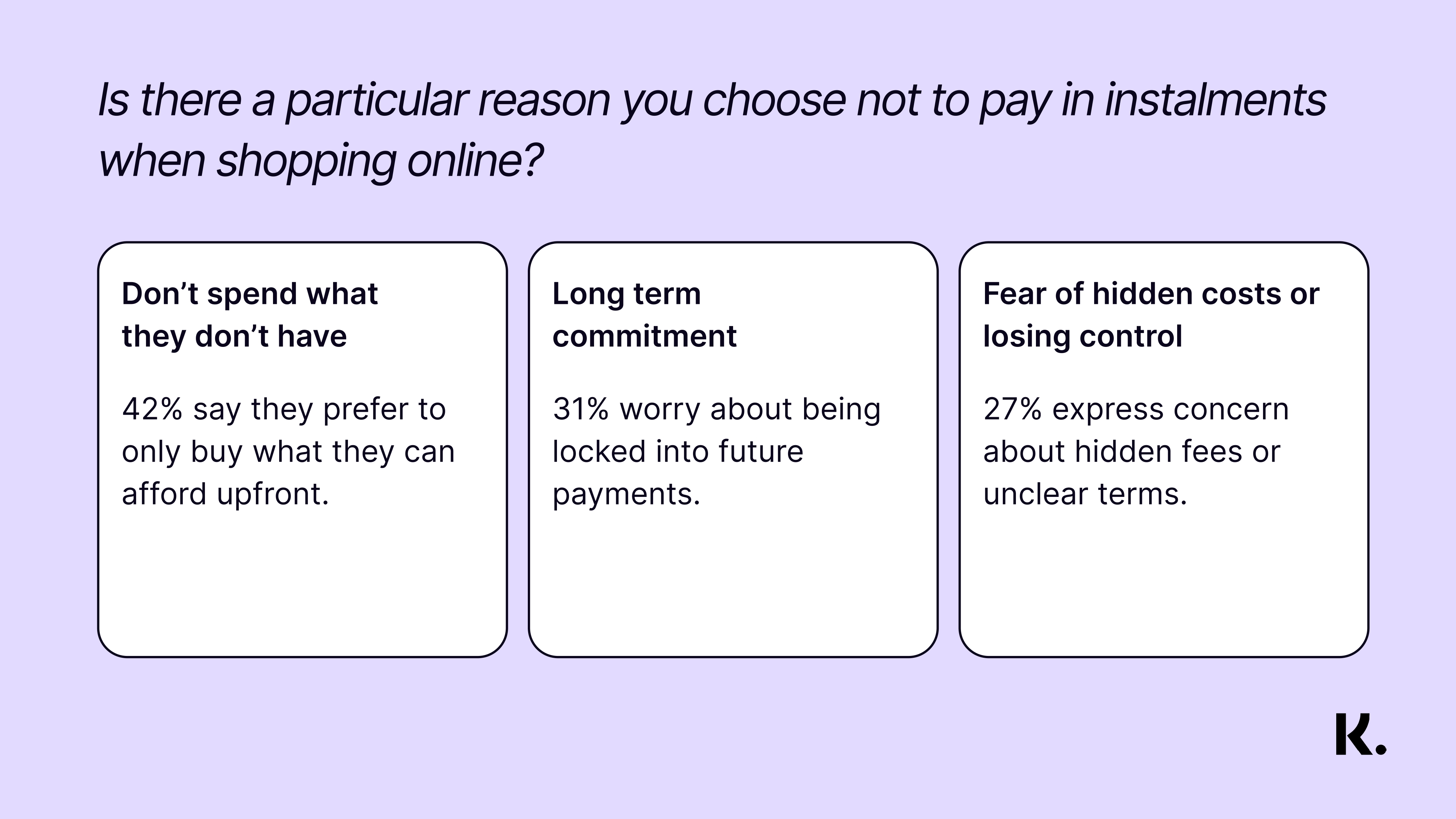

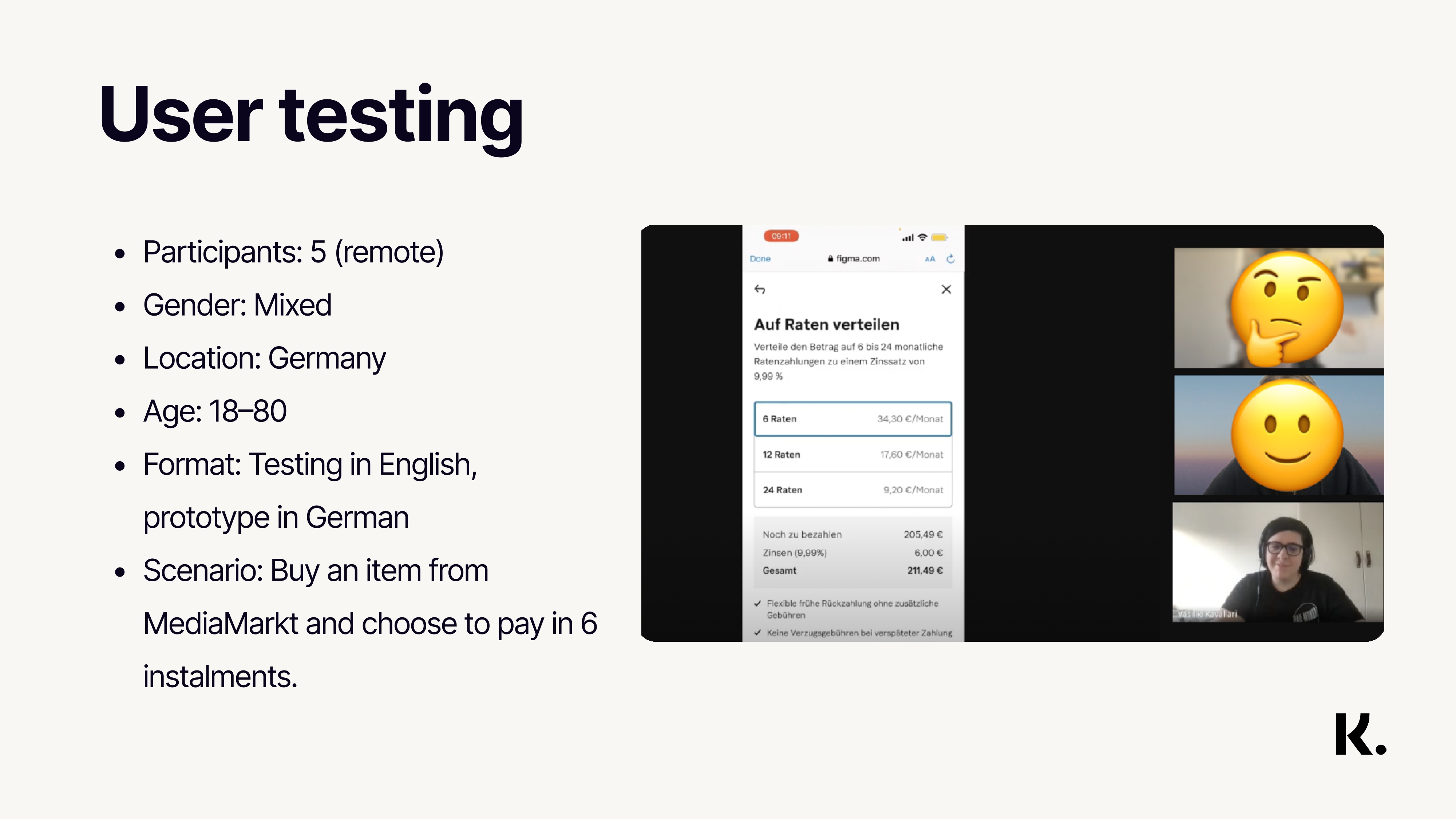

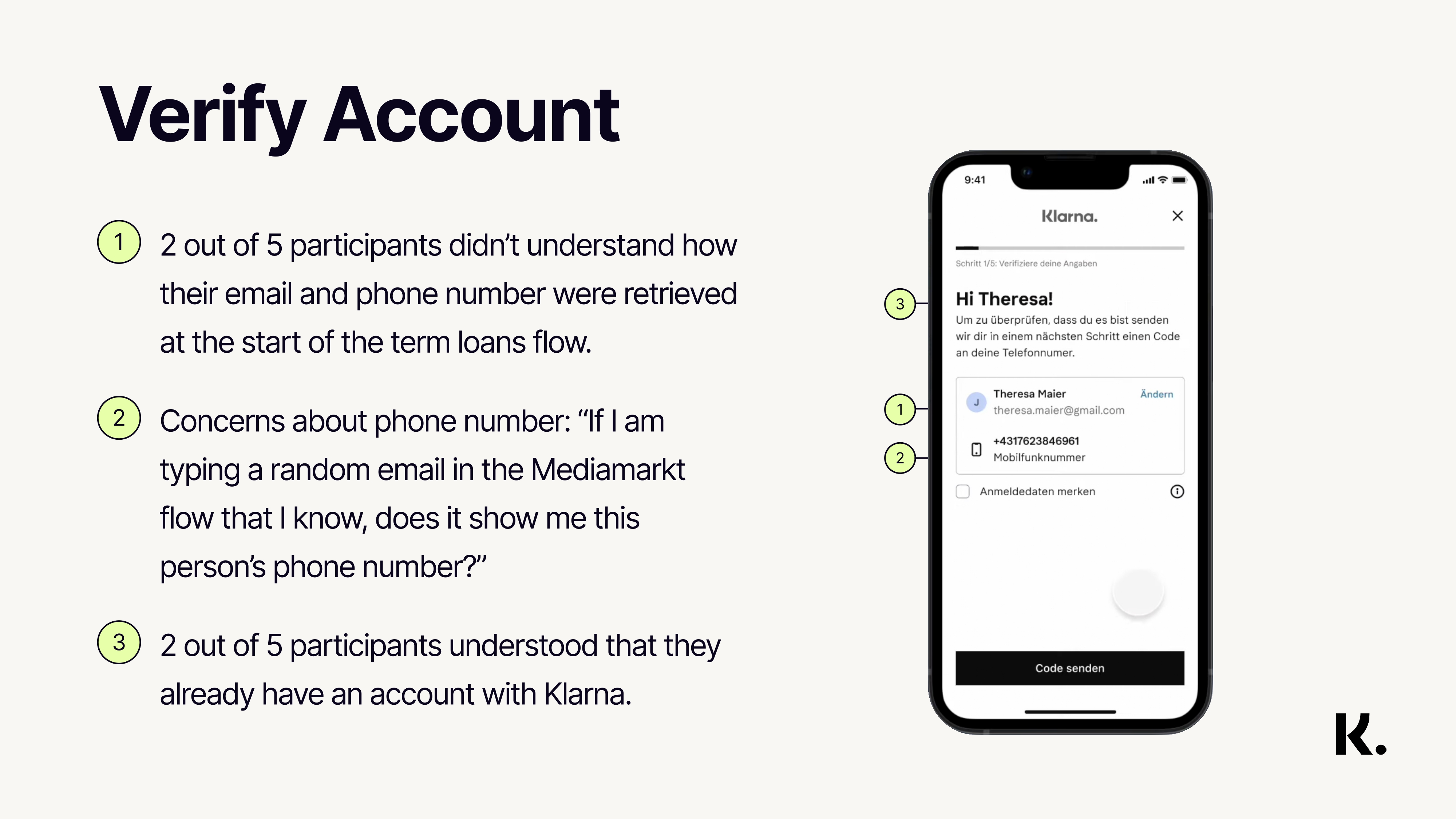

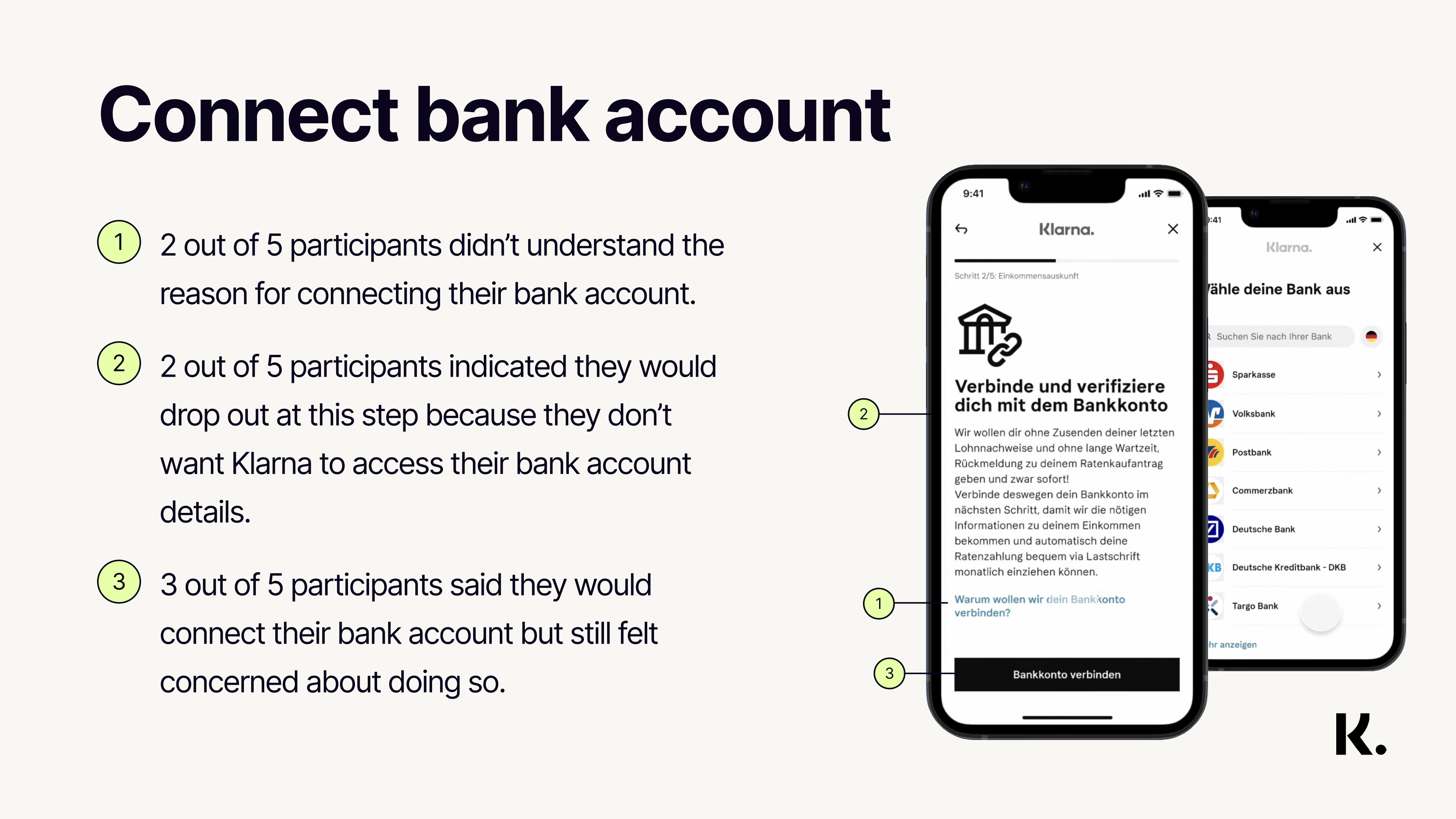

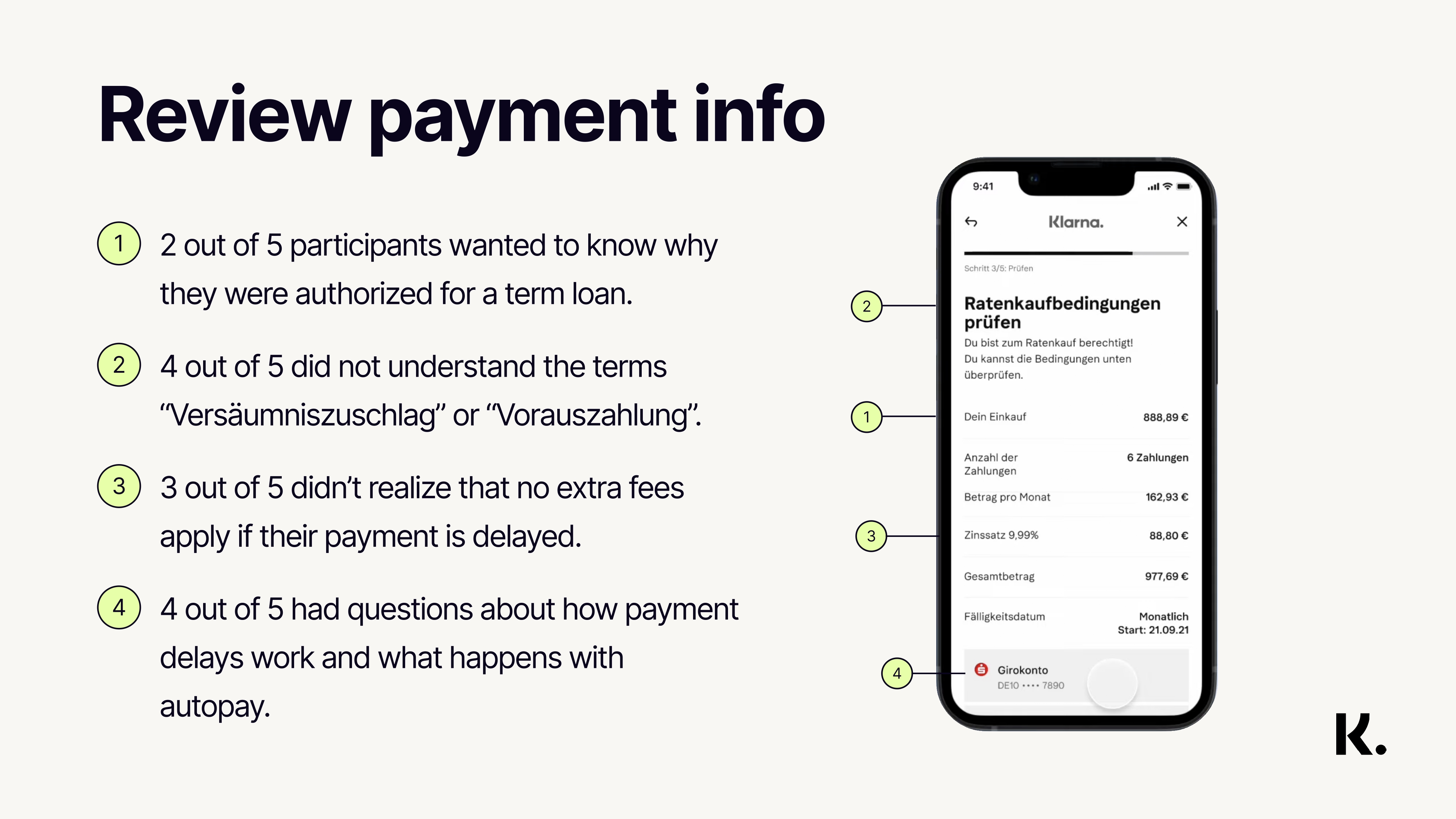

I analyzed Klarna’s financing experiences across Sweden, Germany, the UK, and the US, and benchmarked against PayPal and Affirm. This exposed friction points and inconsistencies we needed to fix. We also surveyed two groups in Austria and Germany: financing users and non-financing users. Then we ran five moderated user tests using TestingTime and Google Meet. Participants completed a realistic purchase flow on MediaMarkt for a washer and dryer paid in six installments.

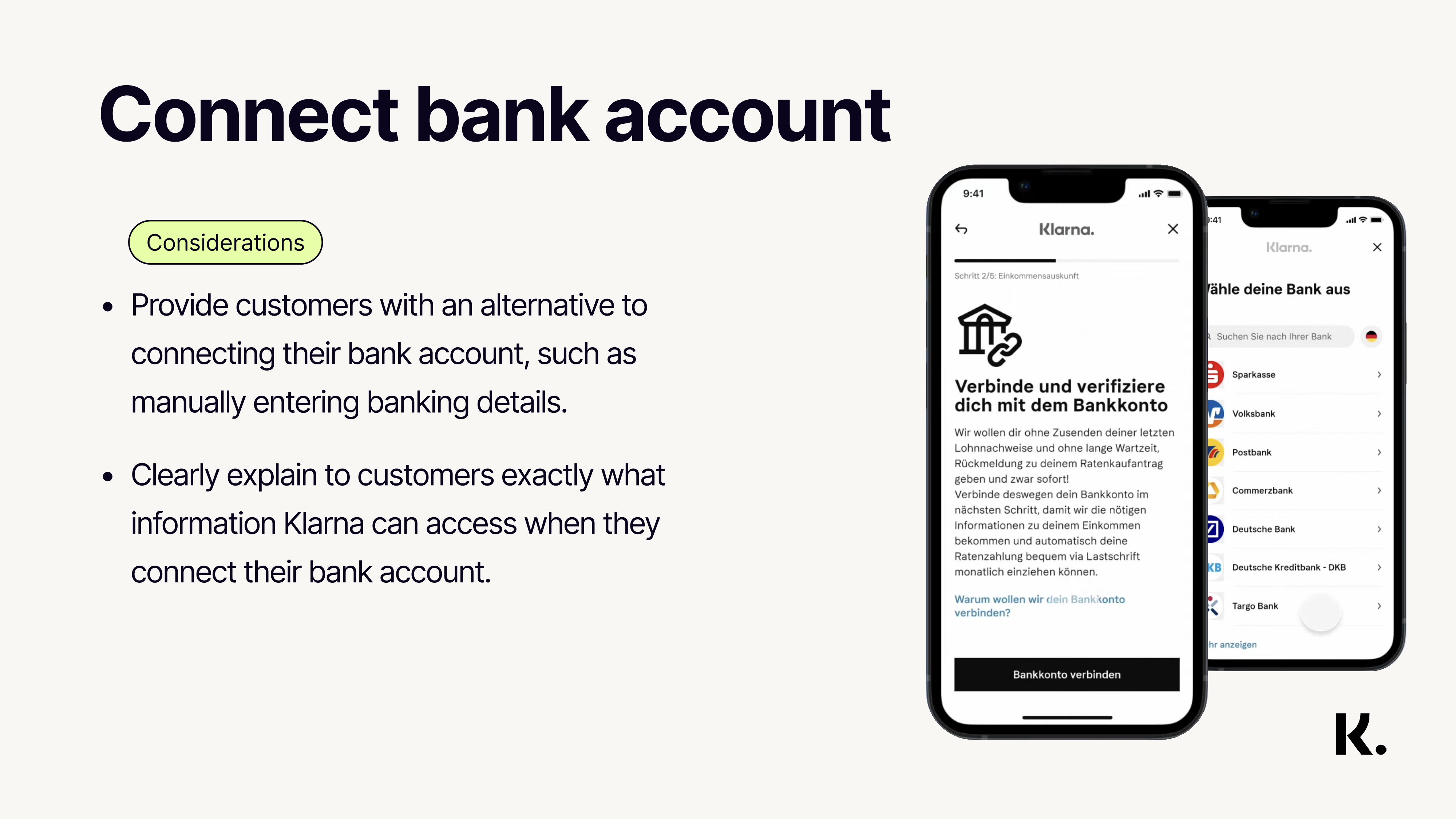

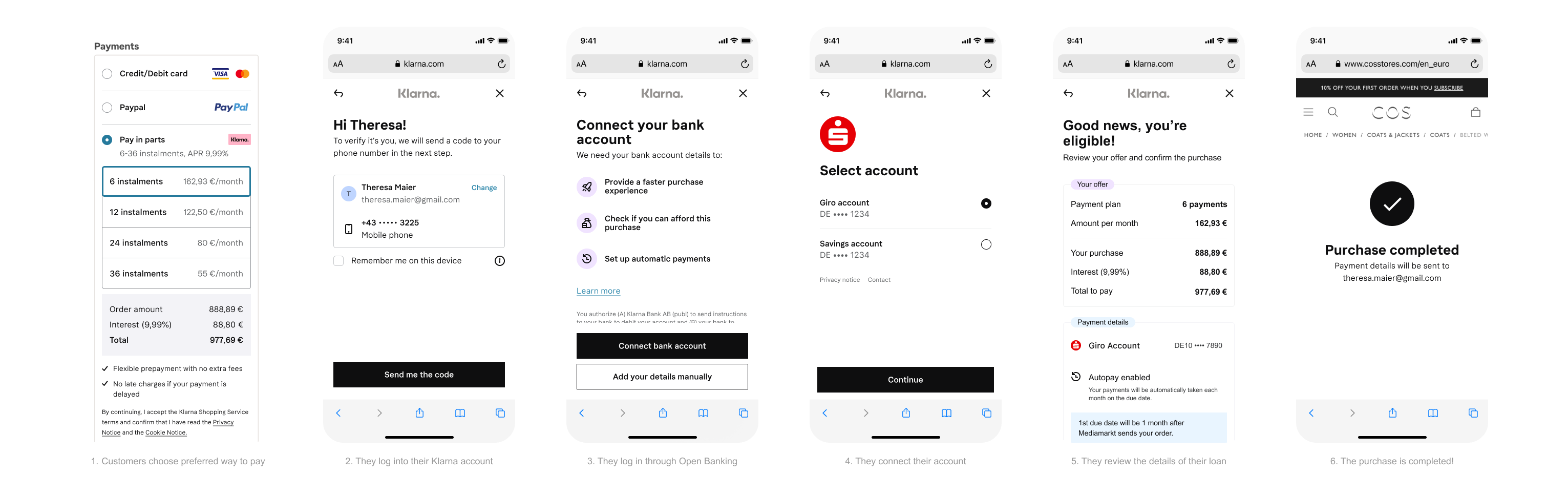

- Add Open Banking integration. Collaborated with another team to let users connect their bank account, verify eligibility, and set up automatic payments in few steps.

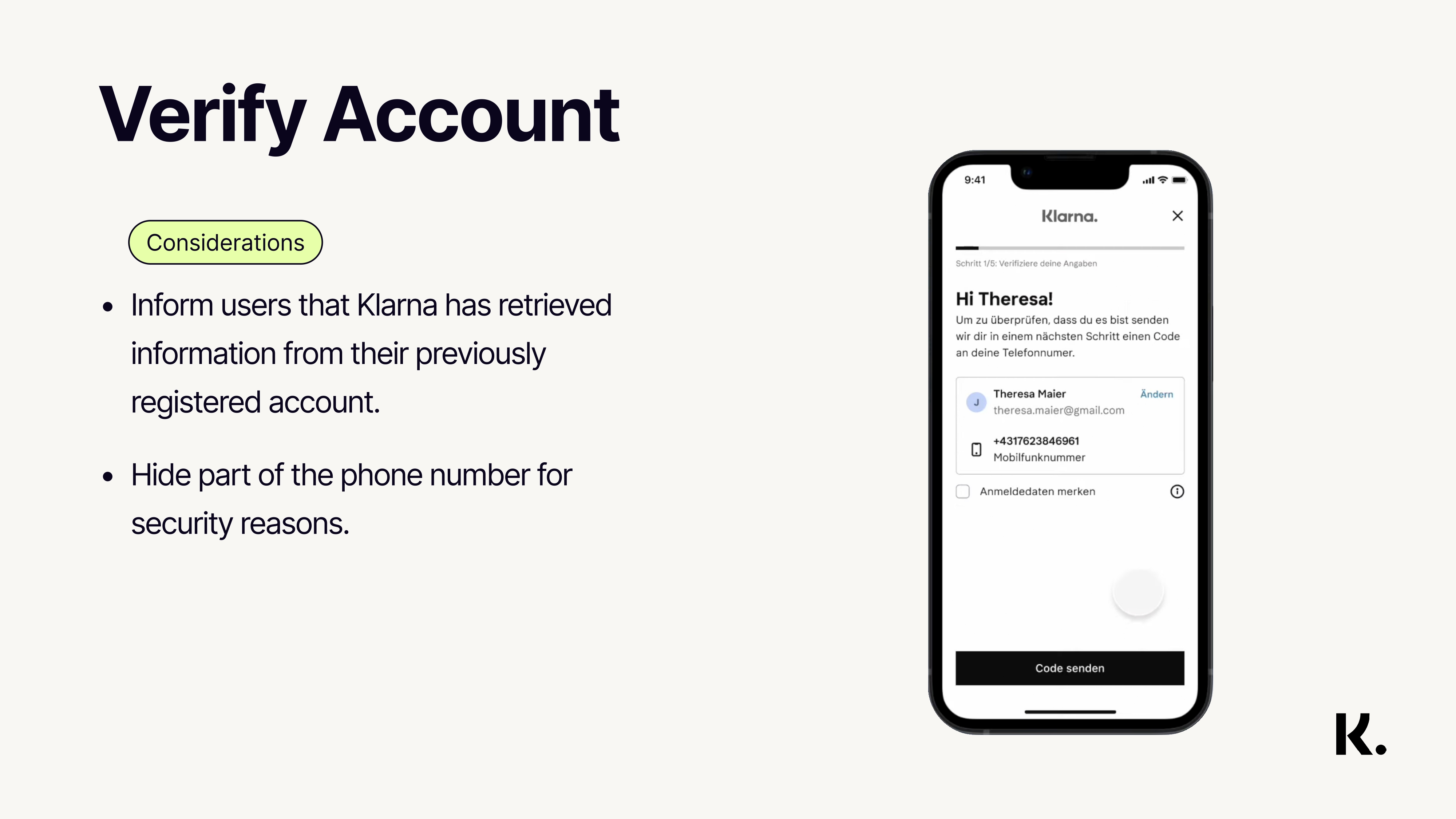

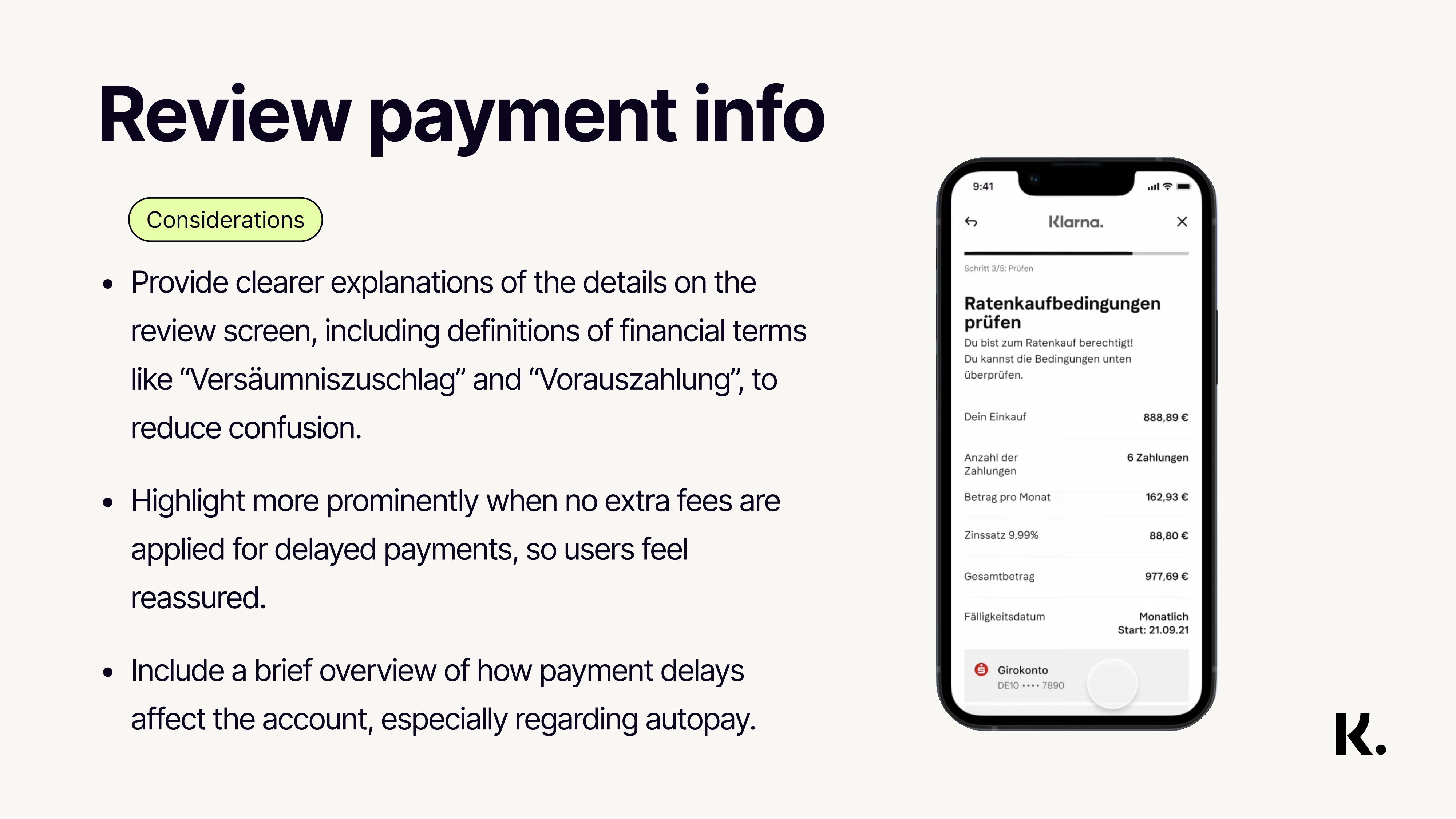

- Increase transparency

Added clear, contextual messages at every stage, explaining why users connect their bank or why a loan might be rejected. - Improve post-purchase updates

Worked with the post-purchase team to improve email and push communication so users receive timely, relevant updates.

We focused on three critical screens: the payment selector, Connect Your Bank Account, and Review screens. These had the highest impact on conversion and user understanding. Weekly design–dev syncs helped iron out edge cases, error handling, and responsive behavior early, reducing rework.

- Rolled out to 200 merchants (50 in Austria, 150 in Germany)

- Reached 85,000 users

- Errand rate (contact support) decreased by 17%

- Funnel drop-offs stayed stable, showing that added transparency didn’t hurt conversion

- Identified new friction: 16% drop-off for purchases under 200€ at the IBAN collection step